The Pricing Engine: Why Your Options Cost What They Do

Most retail traders treat the price of an option as a "suggestion." They see a $500 premium on a BTC call and think, "That looks cheap." It isn't. In the derivatives market, price is an output of a clinical mathematical formula. If you don't understand the inputs, you aren't trading; you're just clicking buttons and hoping the math doesn't catch up to you.

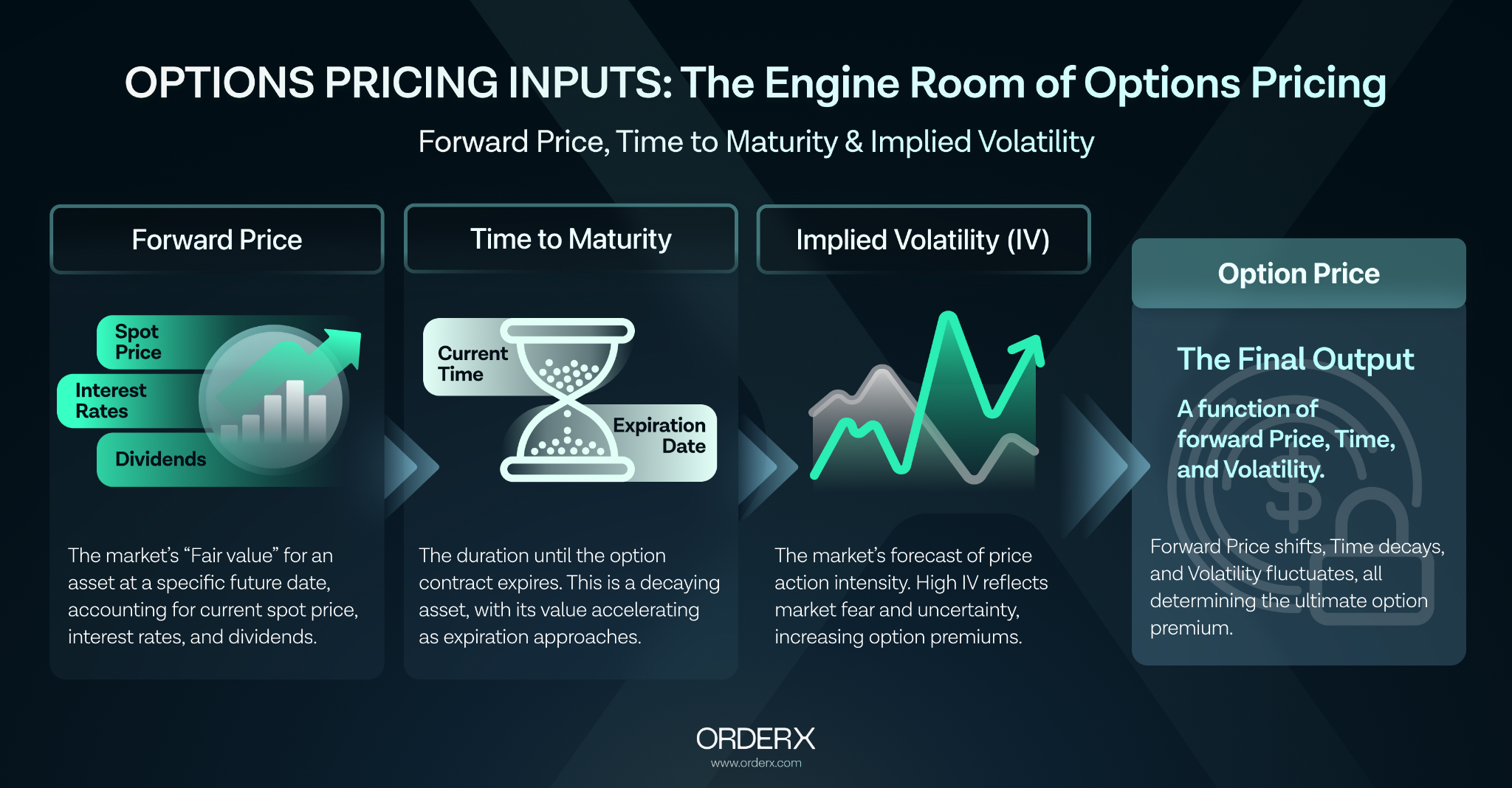

On OrderX, the value of your position is dictated by three primary forces. Ignore them at your peril.

The Forward Price: Trading the Future, Not the Now

Amateurs obsess over the Spot Price (the current price of BTC). Professionals trade the Forward Price.

The Forward Price is the market's "fair value" for BTC at a specific date in the future. It accounts for the spot price, interest rates, and (in traditional markets) dividends. In crypto, this is heavily influenced by the "basis"—the difference between spot and futures prices.

- The Provocation: If you're buying a 3-month BTC call based only on where BTC is today, you're already behind. The market has already priced in the cost of carry.

- The OrderX Reality: Your option is priced relative to where the market expects BTC to be at expiration, not where it’s sitting right now. If the forward price shifts, your option value shifts, even if spot stays dead silent.

Time to Maturity: The Slow Bleed of Theta 𝚹

Time is the only variable in trading that is 100% predictable, yet it’s the one that kills most retail accounts. This is the Time to Maturity.

Every option is a decaying asset. As the expiration date approaches, the "Extrinsic Value" (the premium you paid for the possibility of a move) evaporates. This is known as Theta Θ decay.

- The Mechanic: Decay isn't linear. It accelerates as you get closer to expiration. A 7-day option loses value much faster than a 180-day option.

- The Calculated Risk: Buying "cheap" weekly options is like holding a melting ice cube in a furnace. You aren't just betting that BTC will move; you're betting it will move faster than the clock can kill your position. If BTC goes sideways, the clock wins. Every. Single. Time.

Implied Volatility: The "Fear Gauge"

If Forward Price is the map and Time is the clock, Implied Volatility (IV) is the weather. IV is the market's forecast of how "violent" the price action will be.

IV is the most important component of an option's premium. When the market is terrified, IV spikes, and options become incredibly expensive. When the market is bored, IV crushes, and premiums shrink.

- The Trap: High IV means you are paying a massive "uncertainty tax." If you buy a BTC call during a massive spike in volatility, you might be right about the direction (BTC goes up), but still lose money because the volatility "crushes" after the move, sucking the premium right out of your contract.

- The Pro Move: Professionals don't just trade direction; they trade volatility. They sell options when IV is historically high (collecting fat premiums) and buy them when the market is "asleep" and IV is at the floor.

The Payoff Equation: A Summary for OrderX Traders

Conclusion

Options on OrderX are a game of multi-dimensional chess. If you're only looking at one variable—price—you're playing checkers. To survive, you must respect the Forward price, manage the time to maturity, and price the volatility.